The global lending industry is undergoing a fundamental transformation as artificial intelligence reshapes how financial institutions evaluate borrower risk. For decades, credit decisions were largely dependent on standardized scoring models built on limited financial data such as repayment history and credit utilization. While these models helped banks streamline lending operations, they also introduced constraints that excluded millions of potential borrowers and limited the accuracy of risk assessments. As digital financial services expand and new data sources become available, lenders are increasingly turning to AI-powered credit scoring systems to make more precise, data-driven decisions.

AI-based credit scoring systems analyze a far broader range of financial and behavioral data than traditional models. Instead of relying on static rules, these systems use machine learning algorithms that learn patterns from historical lending data and continuously improve risk predictions. This allows lenders to identify creditworthy borrowers who may not have strong traditional credit histories, while also detecting early warning signals that indicate potential default risk.

The adoption of artificial intelligence in credit scoring is accelerating across banks, fintech startups, digital lenders, and microfinance institutions. According to research published by the World Bank and the International Monetary Fund, AI-driven credit analytics can significantly improve lending accuracy and expand access to financial services for underserved populations. As a result, many financial institutions are investing in AI-powered credit scoring platforms that combine data science, machine learning, and automated decision engines.

Understanding how these systems work begins with examining the foundations of traditional credit scoring and how artificial intelligence enhances those methods.

What Is a Credit Scoring System?

A credit scoring system is a financial risk assessment framework used by lenders to evaluate whether a borrower is likely to repay a loan. The system assigns a numerical score based on a borrower’s credit history and financial behavior. This score helps banks, credit card companies, and lending platforms make consistent decisions about loan approvals, interest rates, and credit limits.

Traditional credit scoring models analyze several financial indicators to determine a borrower’s reliability. These indicators typically include payment history, outstanding debt, credit utilization ratio, length of credit history, and types of credit accounts. The resulting credit score summarizes these factors into a standardized number that lenders use to estimate the probability of default.

One of the most widely used scoring models globally is the Fair Isaac Corporation scoring framework, commonly known as the FICO Score. Another major credit scoring provider is Experian, along with other credit bureaus such as Equifax and TransUnion. These organizations collect credit data from lenders and generate credit reports that form the foundation of traditional credit scoring.

In practice, lenders use these scores to determine loan eligibility. A higher credit score indicates lower risk, which often results in better loan terms and lower interest rates. Conversely, borrowers with low credit scores may face loan rejections or higher borrowing costs due to perceived repayment risk.

While traditional credit scoring systems have played a central role in modern banking, their reliance on limited financial records often prevents lenders from accurately assessing borrowers with little or no credit history.

What Is AI-Based Credit Scoring?

AI-based credit scoring refers to the use of artificial intelligence and machine learning algorithms to evaluate borrower risk using a broader range of data sources and predictive analytics. Unlike traditional credit scoring models that rely on fixed rules, AI-driven systems learn from large datasets and continuously improve their predictive accuracy over time.

Machine learning models analyze patterns across thousands or even millions of historical lending transactions. These algorithms can detect complex relationships between financial behavior and repayment outcomes that traditional statistical models may overlook. As a result, AI-based systems can estimate credit risk more precisely and adapt to changing economic conditions or borrower behavior.

One key advantage of AI credit scoring is the ability to incorporate alternative data sources. In addition to traditional credit bureau information, AI models can analyze bank transaction data, utility bill payments, mobile wallet activity, e-commerce behavior, and other digital financial signals. These data points provide deeper insights into a borrower’s financial habits and stability.

Another important improvement is automation in lending decisions. AI-powered scoring engines can process large volumes of loan applications in real time and generate risk assessments within seconds. This enables financial institutions to deliver faster approvals, reduce operational costs, and scale lending operations efficiently.

The fundamental difference between AI-based scoring and traditional models lies in flexibility. While rule-based systems rely on predefined thresholds and formulas, AI systems dynamically adjust their predictions based on evolving data patterns, resulting in more accurate and adaptive credit risk analysis.

Why Financial Institutions Are Adopting AI Credit Scoring

Financial institutions across the world are rapidly adopting AI-powered credit scoring because it improves lending efficiency, risk management, and market reach. Traditional underwriting processes often require manual verification and lengthy credit evaluations, which slow down loan approvals and increase operational costs. AI systems significantly accelerate these processes by automating data analysis and decision-making.

One of the most immediate benefits of AI credit scoring is faster loan approvals. Digital lenders can evaluate applications within seconds by analyzing large datasets in real time. This capability has become particularly important in online lending platforms, where customers expect instant credit decisions.

AI also improves the accuracy of risk prediction. By analyzing complex behavioral patterns and large historical datasets, machine learning models can detect subtle indicators of creditworthiness that conventional scoring systems may overlook. Studies conducted by the Bank for International Settlements indicate that machine learning models can outperform traditional credit scoring models in predicting borrower defaults when trained on high-quality financial data.

Another major driver of adoption is financial inclusion. Many individuals and small businesses lack formal credit histories, making them invisible to traditional credit scoring systems. AI models can analyze alternative data such as digital payments, mobile transactions, and utility payment behavior to evaluate creditworthiness for these underserved populations.

Finally, AI credit scoring helps reduce default rates by identifying high-risk borrowers earlier in the lending process. Advanced analytics can flag risky financial patterns, enabling lenders to adjust credit limits, interest rates, or loan terms before approving credit.

As lending ecosystems become increasingly digital, AI-based credit scoring is emerging as a critical technology for modern financial institutions seeking to balance growth with responsible risk management.

Limitations of Traditional Credit Scoring Models

Traditional credit scoring systems have been the foundation of lending decisions for decades. Banks, credit card companies, and financial institutions rely on these models to evaluate borrower risk and determine whether an applicant qualifies for a loan. While these systems helped standardize lending processes and reduce manual underwriting, they were built for an earlier era of financial services when digital data was limited and lending decisions relied heavily on historical credit records.

Today’s financial ecosystem has evolved significantly. Digital banking, mobile payments, online commerce, and fintech platforms generate vast amounts of financial data that traditional scoring models cannot fully utilize. As a result, many lenders are recognizing the limitations of legacy credit scoring frameworks. These systems often fail to accurately assess borrowers with limited credit histories and may overlook valuable behavioral signals that indicate financial reliability.

The shift toward AI-powered credit scoring is largely driven by the need for more accurate risk prediction, faster decision-making, and broader financial inclusion. To understand why artificial intelligence is becoming essential in modern lending, it is important to first examine how traditional credit scoring works and where its limitations arise.

How Traditional Credit Scoring Works

Traditional credit scoring models evaluate a borrower’s likelihood of repaying a loan by analyzing historical credit data stored by credit bureaus. These systems use statistical models to assign a numerical score based on several financial indicators derived from an individual’s credit report.

One of the most widely used frameworks is the FICO Score developed by Fair Isaac Corporation. Similar models are also provided by major credit reporting agencies such as Experian, Equifax, and TransUnion. These models rely on predefined formulas that evaluate several key factors to determine a borrower’s creditworthiness.

Payment history is typically the most influential component in traditional credit scoring. Lenders examine whether a borrower has consistently paid loans, credit cards, or other financial obligations on time. Late payments, defaults, or accounts sent to collections negatively impact the score.

Credit utilization is another important factor. It measures how much credit a borrower is using compared to their available credit limits. High utilization ratios often signal financial stress and can lower a credit score.

The length of credit history also plays a role in scoring models. Borrowers with long-established credit accounts provide more historical data for lenders to evaluate, which often results in higher confidence in repayment behavior.

Credit mix refers to the diversity of credit accounts a borrower maintains, such as credit cards, mortgages, auto loans, or personal loans. A balanced mix of credit types suggests responsible financial management and may positively influence the credit score.

While these factors have helped lenders assess borrower risk for many years, the system’s heavy reliance on historical credit activity limits its ability to evaluate individuals with little or no formal credit records.

Key Limitations of Traditional Credit Scoring

Despite their widespread use, traditional credit scoring models face several structural limitations that reduce their effectiveness in modern financial systems. One of the most significant issues is their dependence on a narrow set of data sources. These systems rely primarily on credit bureau records, which include loan repayment histories, credit card usage, and other formal financial transactions reported by lenders.

This limited dataset excludes many forms of financial behavior that may indicate creditworthiness. For example, regular payments for rent, utilities, subscriptions, or digital services are rarely incorporated into traditional credit scoring models. As a result, borrowers who demonstrate responsible financial habits outside the formal banking system may still receive low credit scores.

Another major limitation is the exclusion of individuals with “thin credit files.” Thin-file borrowers are individuals who have little or no recorded credit history. This group often includes young professionals, recent immigrants, gig economy workers, and people in emerging markets who rely more on mobile payments or informal financial systems. Because traditional scoring models require historical credit records, these borrowers may be automatically categorized as high-risk even when they have stable income and reliable payment behavior.

Traditional credit scoring also tends to favor individuals with long-standing relationships with formal banking institutions. Borrowers who have used traditional financial products such as credit cards or bank loans for many years typically receive higher scores. However, this bias can disadvantage populations that primarily rely on digital wallets, peer-to-peer payment platforms, or alternative financial services.

A further challenge lies in the speed of traditional credit assessments. Conventional underwriting processes often require manual review of credit reports and supporting documents. This can slow down loan approvals, especially in large financial institutions where multiple verification steps are required. In contrast, modern digital lending platforms require near-instant decision-making to meet customer expectations.

These limitations highlight why many financial institutions are seeking more flexible and data-driven approaches to credit risk evaluation.

Why AI Improves Credit Risk Assessment

Artificial intelligence offers a fundamentally different approach to credit scoring by addressing the core limitations of traditional models. AI-powered credit scoring systems analyze significantly larger and more diverse datasets, enabling lenders to evaluate borrower risk with greater precision.

One of the most important advantages of AI-based credit scoring is the ability to incorporate alternative data sources. Instead of relying solely on credit bureau records, machine learning models can analyze financial signals from bank transactions, digital payments, mobile wallets, e-commerce activity, and utility bill payments. These additional data points provide a more comprehensive view of a borrower’s financial behavior.

AI systems also support real-time decision-making. Machine learning models can process large volumes of financial data instantly and generate risk predictions within seconds. This capability allows digital lenders to offer immediate credit approvals, which has become a key competitive advantage in fintech platforms.

Another critical benefit is the ability of AI models to continuously learn and improve. Unlike traditional scoring systems that rely on fixed formulas, machine learning algorithms adapt as new data becomes available. When trained on updated lending outcomes, these models refine their predictions and become more accurate over time.

Organizations such as the Bank for International Settlements and the World Bank have highlighted the potential of AI-driven credit analytics to expand financial access while improving risk management. By leveraging advanced analytics, lenders can better identify creditworthy borrowers, reduce default risk, and extend financial services to populations previously excluded from traditional credit systems.

As digital financial ecosystems continue to grow, AI-powered credit scoring is becoming an essential component of modern lending infrastructure.

How AI-Based Credit Scoring Systems Work

AI-based credit scoring systems combine data engineering, machine learning models, and automated decision engines to evaluate borrower risk more accurately than traditional scoring methods. Instead of relying only on credit bureau records, these systems analyze large volumes of financial, behavioral, and transactional data to predict the probability that a borrower will repay a loan.

At a high level, the architecture of an AI-powered credit scoring platform includes four main stages: data collection, data processing, machine learning model prediction, and credit score generation. Each stage transforms raw financial information into structured insights that help lenders assess borrower reliability. Modern fintech platforms and digital banks increasingly rely on these systems because they enable real-time credit decisions, improve risk modeling accuracy, and expand access to financial services.

Understanding how AI-based credit scoring works requires examining each stage of this workflow in detail.

-

Data Collection and Aggregation

The first step in an AI-based credit scoring system is collecting and aggregating data from multiple financial and behavioral sources. Traditional credit scoring models rely primarily on credit bureau reports, but AI systems gather information from a much wider ecosystem of digital data.

One of the most valuable data sources is bank transaction history. By analyzing a borrower’s bank statements, the system can observe patterns such as income stability, spending behavior, recurring expenses, and savings activity. This transactional data provides a detailed view of a borrower’s financial health.

Mobile usage patterns can also provide useful signals for risk assessment, especially in emerging markets where mobile payments and digital wallets are widely used. Frequency of mobile transactions, payment regularity, and mobile wallet balances may indicate financial reliability.

E-commerce activity is another important data source. Online purchase behavior, order frequency, and transaction consistency help lenders evaluate financial discipline and purchasing habits. Digital platforms generate detailed payment records that can supplement traditional financial data.

Utility payment records offer additional insights into a borrower’s reliability. Consistent payments for electricity, internet services, or mobile subscriptions indicate responsible financial behavior even when an individual lacks formal credit accounts.

Some fintech platforms also incorporate social data signals, such as digital identity verification or online presence indicators. While these signals must be handled carefully due to privacy and regulatory considerations, they can contribute to identity validation and fraud detection.

To combine these datasets effectively, financial institutions often integrate information from open banking APIs, payment gateways, and third-party data providers. Organizations such as Open Banking Limited have enabled secure data sharing frameworks that allow financial institutions to access user-permitted financial data from multiple sources.

Once this data is collected, it is aggregated into centralized data systems where it can be processed and analyzed by machine learning models.

-

Feature Engineering and Data Processing

Raw financial data alone cannot be directly used to train machine learning models. Before predictive models can analyze borrower behavior, the data must be cleaned, structured, and transformed into meaningful features that represent financial risk indicators. This process is known as feature engineering.

Data normalization is one of the first steps in this stage. Financial datasets often contain inconsistencies, missing values, or varying formats. For example, transaction amounts may appear in different currencies or formats across different banking platforms. Normalization ensures that all data is standardized and comparable across datasets.

Feature extraction involves identifying patterns and variables that can help predict borrower behavior. Instead of feeding thousands of individual transactions into a model, the system extracts summarized indicators such as average monthly income, spending volatility, transaction frequency, or debt-to-income ratios. These engineered features help the model interpret financial behavior more effectively.

Behavioral analysis is another critical component of feature engineering. AI systems analyze spending patterns, payment regularity, and transaction consistency to detect behavioral indicators associated with reliable borrowers. For instance, individuals who consistently pay bills before due dates or maintain stable cash flow patterns may be considered lower risk.

Advanced feature engineering techniques can also detect complex behavioral signals, such as sudden changes in spending habits or abnormal financial activity. These insights improve the predictive power of machine learning models and enable more accurate credit risk assessment.

Once the data is processed and transformed into structured features, it becomes suitable for training machine learning algorithms that estimate borrower risk.

-

Machine Learning Models for Risk Prediction

The core of an AI-based credit scoring system is the machine learning model that predicts the probability of loan repayment. These models analyze historical lending data to identify patterns associated with successful repayments and loan defaults.

One commonly used algorithm in credit risk modeling is logistic regression. This statistical model estimates the probability that a borrower will default on a loan based on various financial indicators. Logistic regression has been widely used in credit scoring because it is relatively transparent and easy to interpret.

More advanced AI systems use ensemble algorithms such as random forests and gradient boosting models. Random forest models combine multiple decision trees to analyze complex relationships between variables. By aggregating predictions from many trees, the model reduces prediction errors and improves overall accuracy.

Gradient boosting models, including algorithms like XGBoost and LightGBM, are widely used in modern fintech platforms because they perform well with structured financial datasets. These models sequentially improve predictions by correcting errors made by earlier models, resulting in highly accurate risk predictions.

Neural networks are also increasingly used in credit scoring systems, particularly when large datasets are available. These models simulate the way the human brain processes information and can identify complex nonlinear relationships within financial data. Neural networks are especially useful when analyzing large volumes of alternative data such as transaction histories or behavioral signals.

Financial institutions and research organizations such as the Bank for International Settlements have highlighted the growing role of machine learning algorithms in improving credit risk prediction accuracy compared to traditional statistical models.

-

Credit Score Generation and Risk Categorization

After the machine learning model analyzes borrower data, the system generates a credit score that represents the predicted risk level associated with the borrower. This score is typically derived from the model’s estimated probability of default.

Instead of producing only a binary decision such as approve or reject, AI credit scoring systems usually assign borrowers to risk tiers. These tiers categorize applicants based on their predicted likelihood of repayment. For example, low-risk borrowers may receive higher credit limits and lower interest rates, while higher-risk applicants may receive reduced loan amounts or stricter lending terms.

Credit scores are often presented within a defined numerical range. Similar to traditional scoring systems, the range allows lenders to quickly compare borrower profiles and determine eligibility thresholds. However, AI-based scores are generated dynamically using predictive models rather than fixed scoring formulas.

Once the score is generated, the decision engine applies lending policies to determine the final outcome. These policies may include automated approval rules, manual review triggers, or additional verification requirements depending on the risk tier.

Modern digital lending platforms integrate these scoring engines directly into their application workflows, enabling real-time lending decisions. When a borrower submits a loan application, the system processes financial data, runs predictive models, generates a credit score, and produces an approval decision within seconds.

By combining advanced analytics with automated decision engines, AI-based credit scoring systems allow lenders to evaluate borrower risk faster, more accurately, and at much larger scale than traditional underwriting models.

Key Features of an AI-Powered Credit Scoring System

Modern lending platforms require credit scoring systems that can process large datasets, generate accurate risk predictions, and automate lending decisions at scale. AI-powered credit scoring platforms provide this capability by combining machine learning algorithms, financial data integration, and automated decision engines. These systems are designed to evaluate borrower risk more efficiently than traditional scoring models while enabling lenders to make faster and more reliable credit decisions.

A robust AI credit scoring system must include several core features that support the entire lending lifecycle, from data analysis and risk prediction to compliance and fraud detection. These capabilities allow financial institutions to streamline underwriting processes, reduce default risk, and expand access to credit for underserved borrowers. The following features represent the foundational components of a modern AI-powered credit scoring platform.

-

Automated Credit Risk Assessment

Automated credit risk assessment is one of the most important capabilities of an AI-powered credit scoring system. Traditional lending processes often require manual review of credit reports, financial documents, and borrower information. This approach can slow down loan approvals and introduce inconsistencies in risk evaluation. Automated decision engines solve this challenge by analyzing borrower data and generating credit decisions without manual intervention.

In an AI-based system, machine learning models evaluate multiple risk indicators simultaneously, including financial history, transaction behavior, and repayment patterns. The system processes these inputs and calculates a risk score that reflects the probability that a borrower will repay a loan. Based on predefined lending policies, the decision engine can automatically approve, reject, or flag an application for manual review.

Automation significantly improves operational efficiency for lenders. Digital lending platforms can process thousands of applications in real time, enabling financial institutions to scale their operations without increasing underwriting staff. This capability is particularly valuable for fintech companies offering instant loans or buy-now-pay-later services, where borrowers expect quick approval decisions.

Automated credit risk assessment also improves consistency in lending decisions. Since AI models rely on standardized algorithms rather than subjective human judgment, they reduce the likelihood of inconsistent evaluations across different loan applications. As a result, lenders can maintain more uniform risk management practices while accelerating the credit approval process.

-

Alternative Data Analysis

One of the most powerful advantages of AI-based credit scoring is the ability to analyze alternative data sources that traditional credit scoring models cannot fully utilize. Conventional credit systems primarily depend on credit bureau records, which include loan repayment history and credit card usage. However, millions of individuals worldwide lack sufficient credit history to generate reliable scores.

AI-powered credit scoring platforms overcome this limitation by incorporating non-traditional financial indicators into their risk analysis models. These alternative data sources provide a broader picture of a borrower’s financial behavior and stability.

Mobile payment activity is one such indicator. The frequency and consistency of digital wallet transactions can reveal patterns of income flow, spending behavior, and payment reliability. In regions where mobile financial services are widely used, mobile payment data can be a strong predictor of creditworthiness.

Online transaction data also provides valuable insights. E-commerce purchase patterns, subscription payments, and digital marketplace activity can indicate financial stability and consumer behavior trends. Regular online payments demonstrate financial discipline even when formal credit accounts are absent.

Behavioral data analysis further enhances credit risk evaluation. AI systems can analyze patterns such as transaction timing, payment regularity, and spending habits. For example, individuals who consistently pay recurring expenses before due dates or maintain stable monthly cash flows may be considered lower-risk borrowers.

By combining these alternative data sources with traditional financial records, AI-based credit scoring systems can evaluate borrowers more comprehensively and expand access to credit for individuals who would otherwise be excluded from traditional lending frameworks.

-

Real-Time Credit Scoring

Real-time credit scoring enables lenders to evaluate loan applications instantly and deliver immediate decisions to borrowers. In traditional lending systems, credit evaluations may take hours or even days because they require manual verification and sequential data processing. AI-powered systems eliminate these delays by automating the entire risk analysis workflow.

When a borrower submits a loan application, the platform automatically collects relevant financial data through integrated APIs and data sources. Machine learning models then analyze the information within seconds, generating a credit score and risk classification almost instantly.

This capability is especially important for digital lending platforms, where customer experience depends heavily on speed and convenience. Real-time credit scoring allows fintech companies to approve small personal loans, credit lines, or buy-now-pay-later transactions within seconds.

Instant decision systems also benefit lenders by reducing operational costs and enabling high-volume loan processing. With automated real-time analysis, financial institutions can scale their lending services without significantly expanding underwriting teams.

-

Fraud Detection Capabilities

Fraud detection is another essential feature of AI-powered credit scoring systems. Financial institutions face constant threats from fraudulent loan applications, identity theft, and financial manipulation. AI models help detect these risks by analyzing behavioral patterns and identifying anomalies within borrower data.

Machine learning algorithms can examine thousands of financial signals simultaneously, detecting unusual activity that may indicate fraud. For example, sudden changes in transaction patterns, inconsistent identity information, or abnormal device usage may trigger fraud alerts.

Advanced AI systems also analyze behavioral biometrics, such as typing patterns, login behavior, or device fingerprints. These signals help verify the authenticity of borrowers and detect suspicious activities that traditional verification systems may overlook.

Fraud detection models continuously learn from historical fraud cases and adapt to emerging threats. As financial criminals develop new tactics, machine learning algorithms update their detection capabilities based on new data patterns. This adaptive approach helps lenders maintain strong defenses against evolving fraud risks.

Organizations such as the Financial Action Task Force emphasize the importance of advanced analytics in preventing financial crime and improving the security of digital lending platforms.

-

Explainable AI and Decision Transparency

While AI models offer powerful predictive capabilities, financial institutions must also ensure that their credit decisions remain transparent and explainable. Regulatory authorities increasingly require lenders to demonstrate how automated decision systems evaluate borrowers and ensure that these systems do not produce unfair or discriminatory outcomes.

Explainable AI refers to techniques that allow lenders to understand and interpret the factors influencing a credit decision. Instead of operating as opaque “black box” systems, explainable models provide insights into which variables contributed to a borrower’s risk score. For example, the system may indicate that a credit decision was influenced by factors such as income stability, payment history, or debt-to-income ratio.

Regulatory frameworks such as the General Data Protection Regulation emphasize the right of individuals to understand automated decisions that affect them. Financial institutions must therefore ensure that AI models provide clear explanations for loan approvals or rejections.

Explainable AI also supports responsible lending practices. By identifying which variables influence credit decisions, lenders can detect potential bias within their models and adjust algorithms accordingly. This helps ensure fairness in lending and improves trust between financial institutions and borrowers.

Transparency is becoming a critical requirement for AI adoption in financial services. By combining powerful predictive models with explainable analytics, modern credit scoring platforms can meet regulatory standards while maintaining high levels of accuracy in risk prediction.

Types of Data Used in AI Credit Scoring

The effectiveness of an AI-based credit scoring system depends heavily on the quality and diversity of the data used to train and operate its predictive models. Traditional credit scoring systems rely primarily on limited financial records collected by credit bureaus. In contrast, AI-driven platforms analyze a broader range of financial, behavioral, and digital data sources to evaluate borrower risk more accurately.

Modern credit scoring systems use large-scale data aggregation to build a comprehensive financial profile of each borrower. By combining conventional financial records with alternative data sources and behavioral indicators, lenders can gain deeper insights into financial reliability, spending behavior, and repayment capacity. This expanded dataset allows machine learning models to detect patterns that traditional credit scoring models cannot identify.

The data powering AI credit scoring typically falls into four major categories: traditional financial data, alternative financial indicators, behavioral and digital activity signals, and structured data governance processes that ensure reliability and regulatory compliance.

-

Financial Data Sources

Traditional financial data remains one of the most important inputs in AI-based credit scoring systems. These records provide verified evidence of a borrower’s financial history and repayment behavior, forming the foundation for risk assessment models.

Bank statements are a primary data source for evaluating financial health. Transaction histories reveal patterns such as income consistency, recurring expenses, savings activity, and overall cash flow stability. AI models analyze these records to detect financial behaviors associated with reliable borrowers, including regular salary deposits and stable spending patterns.

Loan repayment records are another critical indicator of creditworthiness. Financial institutions track how consistently borrowers repay previous loans, including personal loans, auto loans, mortgages, and other credit products. Borrowers with a strong history of on-time repayments are typically categorized as lower-risk applicants. Conversely, frequent late payments or loan defaults indicate higher credit risk.

Credit card usage also provides valuable insights into financial management behavior. AI systems analyze credit utilization ratios, payment timeliness, and spending habits across credit accounts. For example, individuals who consistently maintain low credit balances and pay their statements in full each month often demonstrate responsible financial behavior.

These traditional financial datasets are typically collected from credit reporting agencies such as Experian, Equifax, and TransUnion. While these sources remain essential, they represent only part of the financial profile needed for modern credit risk assessment.

-

Alternative Data Sources

Alternative data has become one of the most transformative components of AI-based credit scoring. Fintech companies increasingly rely on non-traditional financial indicators to evaluate borrowers who lack extensive credit histories. These datasets provide additional context about financial responsibility and help lenders assess creditworthiness beyond traditional banking records.

Utility payment history is one such data source. Regular payments for electricity, water, internet services, or other household utilities indicate consistent financial discipline. Even though these payments may not appear in traditional credit reports, they demonstrate a borrower’s ability to meet recurring financial obligations.

Rental payment data is also a valuable indicator of creditworthiness. Individuals who consistently pay rent on time often demonstrate reliable financial behavior similar to mortgage borrowers. Incorporating rental payment records into credit scoring models allows lenders to recognize responsible tenants who may not yet have formal credit accounts.

Telecommunications data is another emerging dataset used in credit scoring models. Mobile phone payment records, prepaid recharge frequency, and telecom service usage patterns can provide insights into financial stability. In many emerging markets where mobile payments are widespread, telecom data has become an important proxy for financial reliability.

Online shopping patterns and digital transaction history also contribute to alternative credit analysis. E-commerce platforms generate detailed payment records that reveal consumer spending habits, purchasing frequency, and payment reliability. Regular online purchases combined with consistent payment behavior may indicate financial stability and responsible spending patterns.

Organizations such as the World Bank have emphasized the importance of alternative data in expanding financial access to underserved populations. By incorporating these datasets into credit scoring models, lenders can evaluate borrowers who previously lacked sufficient financial records to qualify for credit.

-

Behavioral and Digital Footprint Data

In addition to financial transactions, AI-based credit scoring systems increasingly analyze behavioral data and digital footprints to assess borrower reliability. These signals help lenders understand how individuals interact with financial platforms and manage their financial responsibilities.

Device usage patterns can provide insights into borrower behavior and identity verification. AI systems may analyze device fingerprints, login frequency, and location consistency to confirm that a loan application originates from a legitimate user. These signals help reduce identity fraud and strengthen credit risk assessment.

Payment habits represent another valuable behavioral indicator. AI models examine patterns such as how frequently borrowers make payments before due dates, whether payments are made automatically or manually, and how consistently individuals maintain financial commitments. These patterns often reveal behavioral traits associated with responsible borrowers.

Online financial behavior also contributes to credit risk analysis. Interactions with digital banking apps, mobile wallets, and payment platforms generate detailed activity records that can be analyzed by machine learning models. For example, consistent usage of digital payment platforms and stable transaction activity may indicate a borrower with reliable financial habits.

Behavioral analytics is particularly useful in cases where traditional credit data is limited. By examining digital activity patterns, AI models can identify signals that help estimate repayment likelihood even when formal credit histories are incomplete.

-

Data Quality and Data Governance

The effectiveness of an AI credit scoring system depends not only on the volume of data collected but also on the accuracy and reliability of that data. Poor data quality can significantly reduce the predictive performance of machine learning models and lead to inaccurate lending decisions. As a result, financial institutions must implement strong data governance frameworks to maintain high-quality datasets.

Data validation is a critical step in ensuring that financial records are accurate and consistent. Automated validation processes check for missing values, duplicate records, and inconsistencies across datasets before the data is used for model training.

Data accuracy must also be maintained through continuous monitoring and verification. Financial institutions often cross-reference data from multiple sources to ensure that borrower information is correct and up to date.

Data cleaning processes further improve data quality by removing corrupted or irrelevant records and standardizing data formats. These processes ensure that machine learning models receive structured datasets that accurately represent borrower behavior.

Regulatory frameworks such as the General Data Protection Regulation emphasize responsible data handling and privacy protection in financial systems. By implementing strong data governance practices, lenders can build reliable AI credit scoring systems that produce accurate predictions while maintaining compliance with financial regulations.

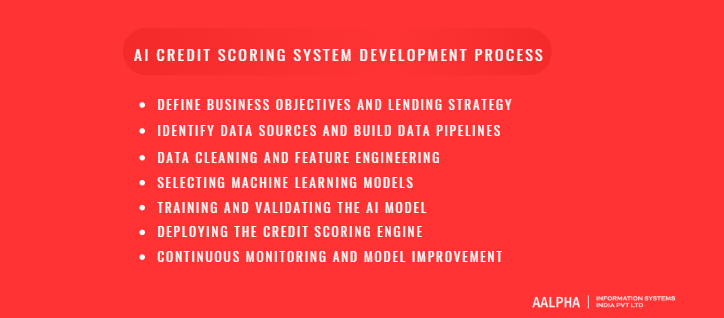

Step-by-Step AI Credit Scoring System Development Process

Developing an AI-based credit scoring system requires a structured approach that combines financial expertise, data engineering, and machine learning development. Unlike traditional credit scoring systems that rely on static formulas, AI-based systems must be designed to continuously learn from new financial data and adapt to changing borrower behavior. This makes the development process more complex but also significantly more powerful.

Financial institutions, fintech startups, and digital lenders typically follow a multi-stage development framework that includes defining lending objectives, building data pipelines, engineering predictive features, selecting machine learning models, and deploying automated decision engines. Each stage plays a critical role in ensuring that the credit scoring system produces accurate and reliable risk predictions.

A well-designed development process not only improves model performance but also ensures regulatory compliance, fairness in lending decisions, and scalability for large-scale lending operations. Many organizations collaborate with an experienced AI development company to accelerate this process, gain access to specialized expertise, and ensure that the platform is built using industry best practices. The following roadmap outlines the key steps involved in building an AI-powered credit scoring platform.

-

Define Business Objectives and Lending Strategy

The first step in building an AI credit scoring system is defining the business objectives and overall lending strategy. Credit scoring models must be aligned with the specific goals of the financial institution, as different lending businesses operate under different risk profiles and market segments.

One of the most important considerations is identifying the target borrower segment. Some lenders focus on prime borrowers with established credit histories, while others specialize in serving underbanked populations who may have limited access to traditional financial services. The characteristics of the target market influence the type of data required and the predictive models used in the scoring system.

The next consideration involves defining the loan products offered by the platform. Credit scoring models may be designed for various lending products such as personal loans, credit cards, small business loans, buy-now-pay-later services, or microloans. Each loan type carries different risk profiles and repayment structures, which must be reflected in the scoring model.

Risk tolerance is another key factor in shaping the credit scoring strategy. Financial institutions must determine the acceptable level of default risk for their lending portfolio. Some lenders prioritize rapid growth and are willing to accept higher default rates, while others prioritize conservative lending policies that minimize financial losses.

By clearly defining borrower segments, loan products, and risk tolerance levels, organizations can design AI credit scoring models that align with their overall business strategy and regulatory requirements.

-

Identify Data Sources and Build Data Pipelines

Once lending objectives are defined, the next step is identifying the data sources that will power the AI credit scoring system. Machine learning models require large volumes of structured financial data to accurately predict borrower behavior, making data acquisition and integration a critical component of system development.

Traditional credit data is typically obtained from credit bureaus and financial institutions. These datasets include information such as loan repayment history, outstanding debts, credit utilization levels, and credit account activity. Credit bureau data provides a reliable baseline for risk assessment because it contains verified financial records.

In addition to traditional credit data, AI credit scoring systems often integrate alternative datasets that provide additional insights into borrower behavior. These datasets may include utility payment records, rental payment histories, telecom billing records, digital wallet transactions, and e-commerce purchase data. Incorporating these alternative indicators allows lenders to evaluate borrowers with limited traditional credit histories.

To collect and process these datasets efficiently, financial institutions must build robust data pipelines that automate data ingestion and storage. Data pipelines typically connect multiple external data providers through secure APIs and stream financial records into centralized data systems for processing.

Open banking frameworks have made it easier for lenders to access financial data directly from banking institutions with customer consent. Organizations such as Open Banking Limited have established secure standards that enable financial institutions to share banking data across platforms while maintaining strong security and privacy protections.

Well-designed data pipelines ensure that AI models receive consistent, real-time financial data, enabling more accurate and up-to-date credit risk predictions.

-

Data Cleaning and Feature Engineering

Before machine learning models can analyze borrower data, the raw datasets must undergo extensive preprocessing to ensure accuracy and usability. This stage involves data cleaning, normalization, and feature engineering to transform raw financial records into meaningful predictive indicators.

Data cleaning removes errors, duplicates, and incomplete records from the dataset. Financial data often contains inconsistencies such as missing transaction entries, incorrect values, or incompatible data formats. Cleaning the data ensures that the machine learning model receives reliable information for training.

Normalization standardizes data across different sources so that values can be compared consistently. For example, financial data collected from multiple banking institutions may use different formats or currencies. Normalization converts these values into a unified structure suitable for machine learning analysis.

Feature engineering transforms raw financial data into structured variables that represent borrower behavior. Instead of analyzing individual transactions, AI systems extract summary indicators such as average monthly income, total monthly spending, debt-to-income ratio, or payment consistency metrics. These engineered features help the machine learning model identify patterns associated with loan repayment or default.

Effective feature engineering significantly improves model performance because it highlights the financial signals most relevant to credit risk prediction.

-

Selecting Machine Learning Models

Selecting the appropriate machine learning model is one of the most important decisions in AI credit scoring development. Different algorithms offer varying levels of interpretability, predictive accuracy, and computational complexity.

Logistic regression remains a widely used model in credit risk analysis because it provides interpretable results and is relatively easy to implement. Many financial institutions use logistic regression as a baseline model for estimating default probability.

Tree-based models such as random forests and gradient boosting algorithms have become increasingly popular in modern credit scoring systems. Random forest models combine multiple decision trees to analyze relationships between borrower variables, improving prediction accuracy while reducing the risk of overfitting.

Gradient boosting algorithms such as XGBoost and LightGBM are widely used in fintech applications because they can handle complex datasets with high predictive performance. These models iteratively refine predictions by correcting errors from previous iterations, allowing them to capture subtle patterns in borrower behavior.

Neural networks represent another advanced modeling approach, particularly when large datasets are available. These models can analyze complex nonlinear relationships in financial data, making them suitable for analyzing alternative data sources and behavioral signals.

When selecting a model, developers must consider several criteria, including prediction accuracy, interpretability, training complexity, and regulatory requirements. Financial regulators often require lenders to explain how credit decisions are made, which means that model transparency is an important consideration.

-

Training and Validating the AI Model

After selecting the machine learning model, the next step is training the model using historical financial data. During the training process, the algorithm learns patterns that distinguish borrowers who repay loans from those who default.

The training dataset typically contains labeled examples of past lending decisions and their outcomes. Each record includes borrower attributes along with a label indicating whether the loan was successfully repaid or defaulted. By analyzing these patterns, the model learns to estimate the probability of default for new borrowers.

Model validation is essential to ensure that predictions remain accurate when applied to new data. Validation techniques such as cross-validation and holdout testing allow developers to measure model performance on datasets that were not used during training.

Bias testing is another critical component of model validation. AI models must be evaluated to ensure that they do not produce unfair outcomes for specific demographic groups. Regulatory frameworks require lenders to ensure fairness and transparency in automated decision systems.

Research institutions such as the Bank for International Settlements have highlighted the importance of robust model validation and bias mitigation when implementing AI systems in financial services.

-

Deploying the Credit Scoring Engine

Once the AI model has been trained and validated, it must be deployed within the financial institution’s lending infrastructure. Deployment involves integrating the credit scoring engine into loan application workflows so that it can evaluate borrowers in real time.

Modern credit scoring systems are typically deployed as scalable services within cloud-based environments. When a borrower submits a loan application, the platform collects relevant financial data, processes the information through the machine learning model, and generates a credit score.

The scoring engine then interacts with automated decision rules that determine the final lending outcome. Applications may be automatically approved, rejected, or routed for manual review depending on the risk score and lending policies.

Integration with loan management systems, customer onboarding platforms, and identity verification tools ensures that the credit scoring system functions seamlessly within the broader lending ecosystem.

-

Continuous Monitoring and Model Improvement

AI credit scoring systems require continuous monitoring and improvement to maintain predictive accuracy over time. Borrower behavior, economic conditions, and financial market trends can change, which may affect the reliability of predictive models.

Performance monitoring tools track key metrics such as prediction accuracy, default rates, and model drift. If the system detects declining model performance, developers may retrain the model using updated datasets.

Periodic model retraining allows the AI system to incorporate new financial behavior patterns and maintain accurate risk predictions. This continuous learning capability is one of the major advantages of AI-based credit scoring compared to traditional static models.

By implementing ongoing monitoring and model improvement processes, financial institutions can ensure that their credit scoring systems remain accurate, fair, and aligned with evolving lending conditions.

Cost of Developing an AI Credit Scoring System

The cost of developing an AI-based credit scoring system varies widely depending on the complexity of the platform, the scale of deployment, and the level of regulatory compliance required. Financial institutions and fintech startups typically view credit scoring technology as a long-term strategic investment because it directly influences lending efficiency, risk management, and profitability.

Unlike traditional credit scoring models that rely on static rules, AI-powered systems require data infrastructure, machine learning development, and continuous model monitoring. Development costs therefore include multiple components such as data acquisition, algorithm design, system integration, and regulatory compliance. The total investment can range from a relatively modest prototype built for a fintech startup to a large-scale enterprise system deployed by a global banking institution.

Understanding the key factors that influence development costs helps organizations plan budgets and evaluate the return on investment of implementing AI-driven credit scoring technology.

-

Factors Affecting Development Cost

Several factors influence the overall cost of developing an AI credit scoring system. One of the most significant cost drivers is data acquisition. Machine learning models require large volumes of financial data to produce accurate predictions. Accessing this data may involve purchasing datasets from credit bureaus, integrating open banking APIs, or partnering with third-party data providers. In many cases, financial institutions must also invest in secure data storage and processing infrastructure to handle these datasets.

Model complexity is another major factor affecting development cost. Basic credit scoring models using simple machine learning algorithms require fewer computational resources and development time. However, more advanced models that analyze alternative datasets or behavioral signals may require complex data pipelines, high-performance computing resources, and specialized data science expertise.

Regulatory and compliance requirements also influence development costs significantly. Financial institutions must ensure that AI-based credit scoring systems comply with consumer protection laws, data privacy regulations, and fair lending standards. For example, regulations such as the General Data Protection Regulation require organizations to implement strong data protection measures and ensure transparency in automated decision-making.

In addition to regulatory compliance, organizations must invest in cybersecurity measures to protect sensitive financial data. Secure data storage, encryption protocols, identity verification systems, and fraud detection tools are essential components of a reliable credit scoring platform. These requirements add to the overall development cost but are critical for maintaining trust and regulatory approval.

-

Estimated Development Cost by System Complexity

The cost of building an AI credit scoring system varies significantly depending on the scale and sophistication of the platform. Financial institutions may begin with a minimum viable product (MVP) and gradually expand the system into a more advanced lending platform.

An MVP credit scoring platform typically focuses on a limited set of features designed to test the viability of the credit scoring model. This type of system may integrate basic financial data sources such as bank transaction records and credit bureau information. The platform may use relatively simple machine learning algorithms and limited automation capabilities. Development of an MVP system generally focuses on building a working prototype that can evaluate borrower risk and support basic lending decisions. The cost of building an MVP AI credit scoring system typically ranges from approximately $50,000 to $120,000 depending on data integration complexity and system architecture.

A mid-scale fintech credit scoring platform includes more advanced features and broader data integration. These platforms often incorporate alternative data sources such as mobile payments, digital wallet transactions, and e-commerce activity. The system may also include automated underwriting engines, fraud detection capabilities, and real-time credit scoring services. Development costs for mid-scale platforms generally range from $150,000 to $400,000 depending on the number of integrations and the sophistication of machine learning models.

Enterprise-level banking solutions represent the most complex and expensive category of AI credit scoring systems. Large banks require highly scalable platforms capable of processing millions of credit evaluations while meeting strict regulatory requirements. These systems often include multiple machine learning models, advanced risk analytics, explainable AI capabilities, and integration with core banking infrastructure. Enterprise implementations may also require extensive data governance frameworks and audit capabilities to satisfy financial regulators. The development cost for enterprise AI credit scoring platforms can range from $500,000 to several million dollars depending on system scale and compliance requirements.

These estimates reflect typical development ranges, but the exact cost will depend on the organization’s technical requirements, regulatory environment, and desired level of automation.

- Ongoing Maintenance and Model Training Costs

Developing an AI credit scoring system is only the first stage of the investment. Maintaining and improving the platform requires ongoing operational costs to ensure that the system continues to produce accurate and reliable risk predictions.

Infrastructure costs represent a major component of ongoing expenses. AI credit scoring systems often rely on cloud-based data processing environments capable of handling large volumes of financial data and real-time credit evaluations. These environments require computing resources, data storage, and network infrastructure that must be continuously maintained.

Data updates are another important operational cost. Machine learning models rely on fresh financial data to maintain predictive accuracy. Financial institutions must regularly update datasets with new transaction records, repayment histories, and behavioral indicators. Maintaining access to these datasets may require ongoing partnerships with data providers and financial platforms.

Model retraining is also essential for maintaining the accuracy of AI credit scoring systems. Over time, borrower behavior, economic conditions, and lending patterns may change. Machine learning models must be retrained periodically using updated data to ensure that predictions remain relevant and accurate.

Continuous monitoring tools are often used to track model performance and detect issues such as model drift or declining prediction accuracy. If performance drops below acceptable thresholds, data scientists must update the model and deploy new versions of the scoring algorithm.

Although these maintenance costs require ongoing investment, they enable financial institutions to maintain a highly adaptive credit scoring system that evolves alongside changes in borrower behavior and financial markets.

Regulatory and Compliance Considerations

AI-based credit scoring systems operate in a highly regulated environment because lending decisions directly affect consumer financial access and economic fairness. Financial institutions must ensure that automated credit assessment systems comply with legal frameworks designed to protect borrowers, prevent discrimination, and maintain transparency in financial services.

Regulatory compliance is particularly important when deploying machine learning models in lending decisions because automated systems can influence large volumes of financial approvals and rejections. Governments and financial regulators require lenders to demonstrate that credit decisions are fair, explainable, and based on reliable financial indicators. Failure to comply with these regulations can result in legal penalties, reputational damage, and restrictions on lending operations.

As AI adoption in financial services continues to expand, institutions must carefully address three major regulatory areas: financial lending regulations, data privacy and security requirements, and transparency standards for automated decision systems.

-

Financial Regulations in Credit Scoring

Financial regulations governing credit scoring aim to ensure that lending decisions are fair, transparent, and non-discriminatory. These regulations prevent financial institutions from using biased criteria that could disadvantage certain groups of borrowers based on factors such as race, gender, ethnicity, or other protected characteristics.

In many countries, fair lending regulations require lenders to apply consistent evaluation standards when assessing loan applications. For example, in the United States, the Equal Credit Opportunity Act prohibits lenders from discriminating against applicants based on protected attributes. Similar consumer protection regulations exist in many jurisdictions around the world.

Consumer protection laws also require lenders to clearly communicate the reasons for loan approval or rejection. Borrowers often have the right to request explanations for adverse credit decisions. When AI-powered credit scoring systems are used, financial institutions must ensure that automated decisions remain transparent and understandable.

Regulatory authorities such as the Consumer Financial Protection Bureau oversee lending practices and enforce compliance with consumer protection standards. These agencies monitor whether financial institutions maintain fair credit evaluation processes and ensure that automated scoring systems do not introduce discriminatory outcomes.

Compliance with financial regulations is therefore a critical requirement when designing AI-based credit scoring systems. Developers must ensure that machine learning models use appropriate variables and avoid factors that could indirectly introduce discriminatory bias.

-

Data Privacy and Security Requirements

AI credit scoring systems rely heavily on personal financial data, which makes data privacy and security a central regulatory concern. Financial institutions must implement strict safeguards to protect sensitive customer information and prevent unauthorized access to financial records.

One of the most widely recognized data protection frameworks is the General Data Protection Regulation implemented by the European Union. This regulation establishes strict rules governing how organizations collect, process, and store personal data. Under GDPR, individuals have the right to know how their data is used and may request access, correction, or deletion of their personal information.

Financial institutions that process payment data must also comply with standards such as Payment Card Industry Data Security Standard. This framework outlines security requirements for protecting payment card information, including encryption protocols, secure data storage, and network monitoring practices.

Data encryption plays a critical role in maintaining financial data security. Sensitive information such as bank account details, transaction records, and personal identification data must be encrypted both during transmission and while stored in databases. Encryption ensures that even if data is intercepted, it cannot be accessed without the appropriate decryption keys.

Secure identity verification systems and fraud prevention tools are also essential components of regulatory compliance. Financial institutions must implement robust authentication processes to ensure that credit applications originate from legitimate users and not fraudulent actors.

By implementing strong privacy and security controls, lenders can protect borrower data while maintaining compliance with global financial data protection regulations.

-

AI Transparency and Bias Mitigation

One of the most complex regulatory challenges in AI-based credit scoring is ensuring transparency and fairness in automated decision-making systems. Machine learning models can sometimes operate as “black boxes,” meaning their internal decision processes are difficult to interpret. Regulators increasingly require lenders to implement explainable AI techniques that make automated decisions understandable to both institutions and borrowers.

Explainable AI methods allow developers to identify which variables influenced a credit decision. For example, a system may indicate that a loan application was rejected due to high debt-to-income ratios or inconsistent payment history. Providing this level of transparency helps lenders comply with regulatory requirements that demand clear explanations for credit decisions.

Bias mitigation is another critical aspect of responsible AI implementation. Machine learning models trained on historical financial data may unintentionally learn patterns that reflect existing societal biases. If not carefully monitored, these patterns could result in unfair outcomes for certain demographic groups.

To address this risk, developers conduct fairness testing during the model development process. Fairness testing involves evaluating model predictions across different population groups to ensure that the system does not systematically disadvantage specific communities.

Ethical lending practices require financial institutions to continuously monitor AI systems for bias and adjust algorithms when necessary. Research organizations such as the Bank for International Settlements have emphasized the importance of responsible AI governance in financial services to maintain trust and stability in digital lending systems.

By implementing explainable AI frameworks, fairness testing procedures, and ethical lending policies, financial institutions can ensure that AI-powered credit scoring systems remain transparent, compliant, and socially responsible.

Challenges in Building AI Credit Scoring Systems

Although AI-powered credit scoring systems offer significant advantages in lending accuracy and operational efficiency, building and deploying these platforms is not without challenges. Financial institutions must navigate complex technical, regulatory, and operational barriers when implementing machine learning models in credit risk assessment.

Many organizations underestimate the complexity involved in collecting high-quality data, ensuring fairness in automated decision-making, and integrating AI systems with existing banking infrastructure. These challenges can affect the reliability of predictive models and delay large-scale adoption of AI in lending operations.

Understanding these obstacles in advance allows financial institutions and fintech companies to design better development strategies and mitigate potential risks during system implementation.

-

Data Availability Challenges

One of the most significant challenges in building AI-based credit scoring systems is obtaining high-quality and comprehensive datasets. Machine learning models require large volumes of reliable financial data to generate accurate predictions. However, many financial institutions struggle with fragmented or incomplete data sources.

In traditional banking environments, customer financial data may be distributed across multiple internal systems, including loan management platforms, payment processing systems, and customer databases. Integrating these datasets into a unified data pipeline can be technically complex and time-consuming.

The challenge becomes even greater when evaluating borrowers with limited credit histories. Many individuals, particularly in emerging markets or among younger demographics, may not have sufficient financial records to support conventional risk assessment. This lack of historical credit data makes it difficult to train predictive models capable of accurately evaluating new borrowers.

Financial institutions often address these limitations by incorporating alternative datasets such as digital payments, utility bills, and transaction records from financial technology platforms. Organizations such as the World Bank have highlighted the importance of expanding financial data sources to support more inclusive credit evaluation systems.

-

Model Bias and Fairness Concerns

Another major challenge in AI credit scoring systems involves ensuring fairness and preventing algorithmic bias. Machine learning models learn patterns from historical data, which means that existing social or financial inequalities reflected in historical lending records may influence the model’s predictions.

If historical datasets contain biased patterns, AI models may unintentionally replicate those biases. For example, certain demographic groups may have historically received fewer loan approvals due to limited access to financial services. When machine learning algorithms are trained on such data, they may incorrectly interpret these patterns as indicators of higher credit risk.

Regulatory authorities require lenders to ensure that automated credit decisions do not discriminate against protected groups. To address this issue, developers must implement fairness testing during the model development process. This testing evaluates whether the model’s predictions differ significantly across demographic groups and identifies potential bias in the algorithm.

Techniques such as explainable AI, bias detection algorithms, and balanced training datasets help mitigate these risks. Regulatory institutions and research organizations such as the Bank for International Settlements have emphasized the importance of transparency and fairness in AI-based financial decision systems.

-

Integration with Legacy Banking Systems

Integrating AI credit scoring platforms with existing banking infrastructure is another significant challenge for financial institutions. Many banks operate on legacy core banking systems that were designed decades ago and were not built to support advanced data analytics or real-time machine learning applications.

Legacy systems often rely on outdated database structures and limited integration capabilities. These systems may not support modern APIs or cloud-based data processing environments required for AI models to function efficiently. As a result, integrating machine learning engines into existing lending workflows can require extensive system modernization.

Another challenge arises from the need to connect AI models with multiple operational systems within a bank’s technology stack. Credit scoring engines must communicate with customer onboarding platforms, loan management systems, identity verification services, and fraud detection tools. Ensuring smooth data exchange between these systems requires careful architecture design and secure integration protocols.

Many financial institutions address this challenge by implementing middleware layers or adopting microservices-based architectures that allow AI models to interact with legacy systems without replacing them entirely. However, such integration projects require significant technical expertise and careful system planning.

Overcoming these integration challenges is essential for organizations that want to successfully deploy AI-powered credit scoring systems within large-scale financial environments.

How to Choose the Right AI Development Partner

Building an AI-based credit scoring system requires a combination of financial domain knowledge, advanced data science capabilities, and strong regulatory awareness. For many financial institutions and fintech startups, partnering with an experienced AI development company is the most efficient way to design and deploy such a complex platform. However, selecting the right development partner requires careful evaluation because the quality of the technology partner directly affects the reliability, scalability, and compliance of the final system.

A well-qualified development partner should not only have technical expertise in artificial intelligence and machine learning but also a deep understanding of financial services infrastructure and credit risk modeling. Lenders must assess multiple factors when evaluating potential partners, including their industry experience, technical capabilities, regulatory expertise, and ability to provide long-term support.

The following criteria can help organizations identify the most suitable AI development partner for building a credit scoring platform.

-

Fintech and AI Development Expertise

The first factor to evaluate when selecting an AI development partner is their experience in fintech and financial technology solutions. Credit scoring systems operate within highly regulated financial environments, which means developers must understand lending workflows, risk modeling practices, and financial compliance standards.

Companies with prior experience building fintech platforms are better equipped to design systems that integrate with banking infrastructure, digital lending platforms, and financial data providers. They are also more familiar with industry-specific challenges such as borrower risk assessment, loan underwriting automation, and real-time financial data processing.

An experienced development partner should be able to demonstrate previous work in financial software development, including AI-driven analytics platforms, digital banking systems, or lending automation tools. Case studies, technical documentation, and client references can provide valuable insights into their expertise.

Financial institutions should also evaluate whether the development partner understands modern financial data ecosystems, including open banking frameworks, digital payment networks, and alternative data sources used in AI-based credit scoring.

-

Data Science and Machine Learning Capabilities

AI credit scoring systems rely heavily on advanced data science techniques and machine learning algorithms. Therefore, a strong development partner must have a skilled team of data scientists, machine learning engineers, and data engineers capable of designing predictive models for financial risk assessment.

The development team should have experience working with structured financial datasets, feature engineering techniques, and machine learning algorithms commonly used in credit risk modeling. These include statistical models such as logistic regression as well as advanced machine learning techniques such as gradient boosting and neural networks.

Equally important is the ability to build scalable data pipelines and infrastructure that support continuous model training and real-time credit evaluation. Without robust data engineering capabilities, even the most sophisticated machine learning models cannot operate effectively.

-

Security and Regulatory Compliance Experience

Because credit scoring systems process sensitive financial information, security and regulatory compliance must be central considerations when choosing a development partner. Financial institutions must ensure that the technology platform complies with global data protection regulations and financial security standards.

A qualified AI development partner should have experience implementing data privacy frameworks such as the General Data Protection Regulation and payment security standards like the Payment Card Industry Data Security Standard. These frameworks establish strict requirements for data encryption, access control, and secure data storage.

The development partner should also understand compliance requirements related to fair lending and explainable AI. Credit scoring models must provide transparency in automated decision-making to satisfy regulatory expectations and maintain trust with borrowers.

-

Long-Term Platform Support

AI credit scoring systems require ongoing monitoring, model retraining, and infrastructure maintenance. Choosing a partner that offers long-term support ensures the platform continues to evolve as financial data patterns and regulatory requirements change. Experienced fintech development firms such as Aalpha Information Systems provide continuous system optimization, model updates, and technical support to maintain reliable credit scoring performance over time.

Final Thoughts

AI-based credit scoring systems are transforming how financial institutions evaluate borrower risk. By combining machine learning, alternative data analysis, and automated decision engines, lenders can assess creditworthiness more accurately, approve loans faster, and expand access to financial services for underserved populations. As digital lending continues to grow, AI-powered risk assessment will play a critical role in improving credit decision accuracy, reducing default rates, and enabling scalable lending operations.